Yield curve out of sync with economic momentum

Gold/ silver rate, ISM and IFO are pointing to much flatter yield curves than we see at the moment. Quantitative easing is still pegging the short dated yields at lower levels than otherwise should have been the case, triggering very steep yield curves because of pricing in that central banks are behind the curve.

Japan

The earthquake will bring money back to Japan, but strength of the yen is uncertain because the Bank of Japan will have to step up quantitative easing. The problem for Japan to find profitable infrastructure investments is solved for the time being. Toyota will have to build more new cars (but import them from abroad). One should not overestimate the growth stimulus from the earthquake. Damage repair will take money away from investments that should have be done otherwise. But the damage repair could help to improve the confidence of Japan that it can do some things really good, as for the time being seems the case (the help from government is many times better than after the Kobe earthquake, the nuclear meltdown problems are way better treated than Harrisburg/ Chernobyl, the damage to buildings is incredibly low because of uge advances in earthquake proof building). The reaction of Wall Street Friday on the earthquake was as if it were a non event.

Maybe the influence is not that big on markets. It should cause a touch higher bond yields, lower prices for some Japanese stocks but also higher growth expectations for Japan that could translate into higher share prices.

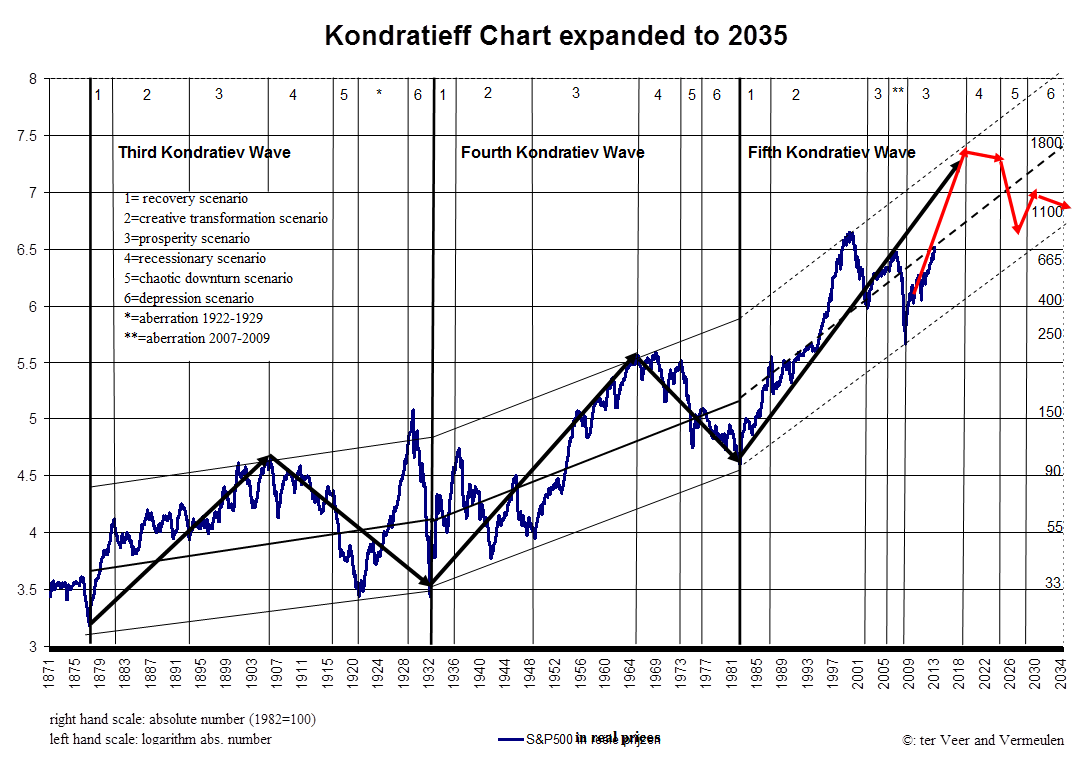

Investment Chart Kondratiev Wave

Sunday 13 March 2011

Mr Market and oil, copper

quities are reacting negatively on higher oil prices, after a long period the opposite happened. This is caused by the market seeing higher risks when oil prices rise above certain levels (+50% in six months is often mentioned as trigger for bad times) and triggering lower growth. Until recently higher oil prices were seen as sign that economic growth was accelerating.

That view is confirmed by Dr. Copper. The copper prices were rising very closely in line with the oil prices until recently. The last weeks you see clearly falling copper prices and higher oil prices (see chart FT): the higher oil prices will cause lower economic growth, so demand for copper will go down as the market is now discounting in the oil prices.

Dr. Copper gives more attention to China and other Emerging Markets than to the US/Europe, so Dr. Copper is saying economic growth will be a bit lower in China/ Emerging Markets than previously thought (e.g. China not growing 10%+ but 8-9%)).

The market is not seeing the rise of the oil prices as permanent. Backwardation has returned in the oil prices, discounting somewhat lower prices after a short period from now.

The share prices of global energy are suddenly breaking down despite the high oil prices, meaning the oil price is not seen to go up from current levels because it will trigger lower economic growth.

The stock markets in the Middle East are in recovery mode, signalling that they fear a lot less potential contagion from the Jasmine Revolution to Saudi Arabia/ severe oil production disruptions.

Sunday 27 February 2011

BCA: no stagflation, Emerging markets have inflation problem that they export to the West

BCA had a special on inflation. Economics has not found out if the current situation of excessive money growth, high increase in commodity prices and high output gap should lead to more inflation.

The relationship between money growth and inflation is away for more than twenty years in the U.S. iso the Fed gives little attention to money growth. The velocity of money has been erratic in yhat period, unpredictable. In the US the correlation between money groth and credit growth not very high (in Europe it was higher, maybe because the short rate of the ECB was less below normal).

Central banks will only wake up when you see strong credit growth (at a certain moment there will be a sudden acceleration when the trust of business is big enough to spend: when they see the competition is brave, fiscal help will disappear, they will follow soon). Then the FED will hike rates, presumably late.

The rise of food prices will lead to only very small rise of the CPI in the US. A 10% rise of commodity prices for food will rise to 4.3% rise of producer prices of food products and they will charge only 1.8% higher prices in the end products of food in the US and that wil lead to 0.7% higher food prices in the supermarkets and that will lead to only a 0.1% higher CPI in the US.

The output gap is still huge in the West and because of that the rise of wages will remain very low, people (and unions) don't dare to ask for higher wages because of higher food and oil prices (unlike in the seventies). That is why you will not see stagflation. The underlying rise of productivity is very high and that also will cause only limited inflation. Because the the rise of unit labour costs lags inflation, one should not be that assured from low unit labour cost growth keeping inflation down.

BCA concludes that inflation in the West will not rise much, especially when core inflation will remain between 1 and 2%, as probably will be the case in the US for the time being.

In emerging markets the inflaton story is completely different. There they have a real inflation problem. High monetary growth is leading to higher inflation (unstoppable as long as they peg their currencies to the dollar and so cause a tremendous growth of foreign currency reserves). The food prices are a big problem because they have a much higher weight in their CPI's and commodity prices are translated much earlier in higher CPI because they have more basic food (not the luxury deserts with lots of marketing costs of the West etc). Because in emerging markets the output gap often is negative you will see high wage demands because of the high food prices.

In the end that will lead to higher export prices, even higher commodity prices and higher inflation everywhere in the world.

My opinion: for the time being inflation will remain moderate, because the rise of productivity will remian high, especuially in emerging markets and in the West the rise of wages will remian limited. But there are several mechanisms that can lead to sudden rises of inflation. Until certain levels monetary growth will not lead to inflation, the big output gaps also help and that will keep infation because of higher commodity prices limited. But when you surpass the safe money growth levels,the output gap in the world is closed (because of emerging markets) inflation kan rise a lot. Suddenly wages will rise to compensate higher gasoline and food prices, credit growth can explode suddenly. The stronger and stronger divide between income growth of the upper class versus the middle class in the West can force highly inflationary wage growth of the upperclass (especially when after that the middleclass doesnt take it any longer and also forces higher wages).

The relationship between money growth and inflation is away for more than twenty years in the U.S. iso the Fed gives little attention to money growth. The velocity of money has been erratic in yhat period, unpredictable. In the US the correlation between money groth and credit growth not very high (in Europe it was higher, maybe because the short rate of the ECB was less below normal).

Central banks will only wake up when you see strong credit growth (at a certain moment there will be a sudden acceleration when the trust of business is big enough to spend: when they see the competition is brave, fiscal help will disappear, they will follow soon). Then the FED will hike rates, presumably late.

The rise of food prices will lead to only very small rise of the CPI in the US. A 10% rise of commodity prices for food will rise to 4.3% rise of producer prices of food products and they will charge only 1.8% higher prices in the end products of food in the US and that wil lead to 0.7% higher food prices in the supermarkets and that will lead to only a 0.1% higher CPI in the US.

The output gap is still huge in the West and because of that the rise of wages will remain very low, people (and unions) don't dare to ask for higher wages because of higher food and oil prices (unlike in the seventies). That is why you will not see stagflation. The underlying rise of productivity is very high and that also will cause only limited inflation. Because the the rise of unit labour costs lags inflation, one should not be that assured from low unit labour cost growth keeping inflation down.

BCA concludes that inflation in the West will not rise much, especially when core inflation will remain between 1 and 2%, as probably will be the case in the US for the time being.

In emerging markets the inflaton story is completely different. There they have a real inflation problem. High monetary growth is leading to higher inflation (unstoppable as long as they peg their currencies to the dollar and so cause a tremendous growth of foreign currency reserves). The food prices are a big problem because they have a much higher weight in their CPI's and commodity prices are translated much earlier in higher CPI because they have more basic food (not the luxury deserts with lots of marketing costs of the West etc). Because in emerging markets the output gap often is negative you will see high wage demands because of the high food prices.

In the end that will lead to higher export prices, even higher commodity prices and higher inflation everywhere in the world.

My opinion: for the time being inflation will remain moderate, because the rise of productivity will remian high, especuially in emerging markets and in the West the rise of wages will remian limited. But there are several mechanisms that can lead to sudden rises of inflation. Until certain levels monetary growth will not lead to inflation, the big output gaps also help and that will keep infation because of higher commodity prices limited. But when you surpass the safe money growth levels,the output gap in the world is closed (because of emerging markets) inflation kan rise a lot. Suddenly wages will rise to compensate higher gasoline and food prices, credit growth can explode suddenly. The stronger and stronger divide between income growth of the upper class versus the middle class in the West can force highly inflationary wage growth of the upperclass (especially when after that the middleclass doesnt take it any longer and also forces higher wages).

Subscribe to:

Posts (Atom)